Yeah, I know, I’m being excessively clever, like the time in my multi-employer pension plan rabbit hole series (to be revisited soon!) that I proclaimed Central States to be fully-funded, because, in addition to the troubled, nearly-insolvent plan by that name, another plan with the same exists, is 108% funded, and offers some instructive comparisons.

And with respect to healthcare, too: every Democratic presidential candidate and all manner of interest groups have proposals for “Medicare for All,” though, by and large, they don’t actually intend to simply provide the same benefit provisions as Medicare includes (Part A deductibles, Part B coinsurance, Part C Medicare Advantage, Part D drugs) to the under-65 American population, but have concluded that it’s a way of speaking about a public healthcare system/single-payer system that generates more positive polling than the words “public healthcare system” or “single-payer system.”

A recent article that came across my twitter feed purports to be “The Only Guide to ‘Medicare for All’ That You Will Ever Need” and differentiates between what it deems to be the “bad” M4A bills, which allow some sort of buy-in to Medicare or Medicaid or another “public option,” and the “good” M4A bills. To meet author Timothy Faust’s requirements, such a program must compel all residents to participate, ban any sort of private health insurance, and cover every form of health/medical care, including “medical, dental, mental, vision, reproductive, long-term, and more,” and Faust notes that “long-term” encompasses all forms of elder care, including in-home services; the system’s expenses would be managed by “negotiation” (which the article itself makes pretty clear means dictating prices to providers).

And Faust acknowledges that this exceeds the norm in the rest of the world, but makes the expansive claim that “we are capable of, and should, provide a higher standard of care than any currently-existing single-payer program on the globe.”

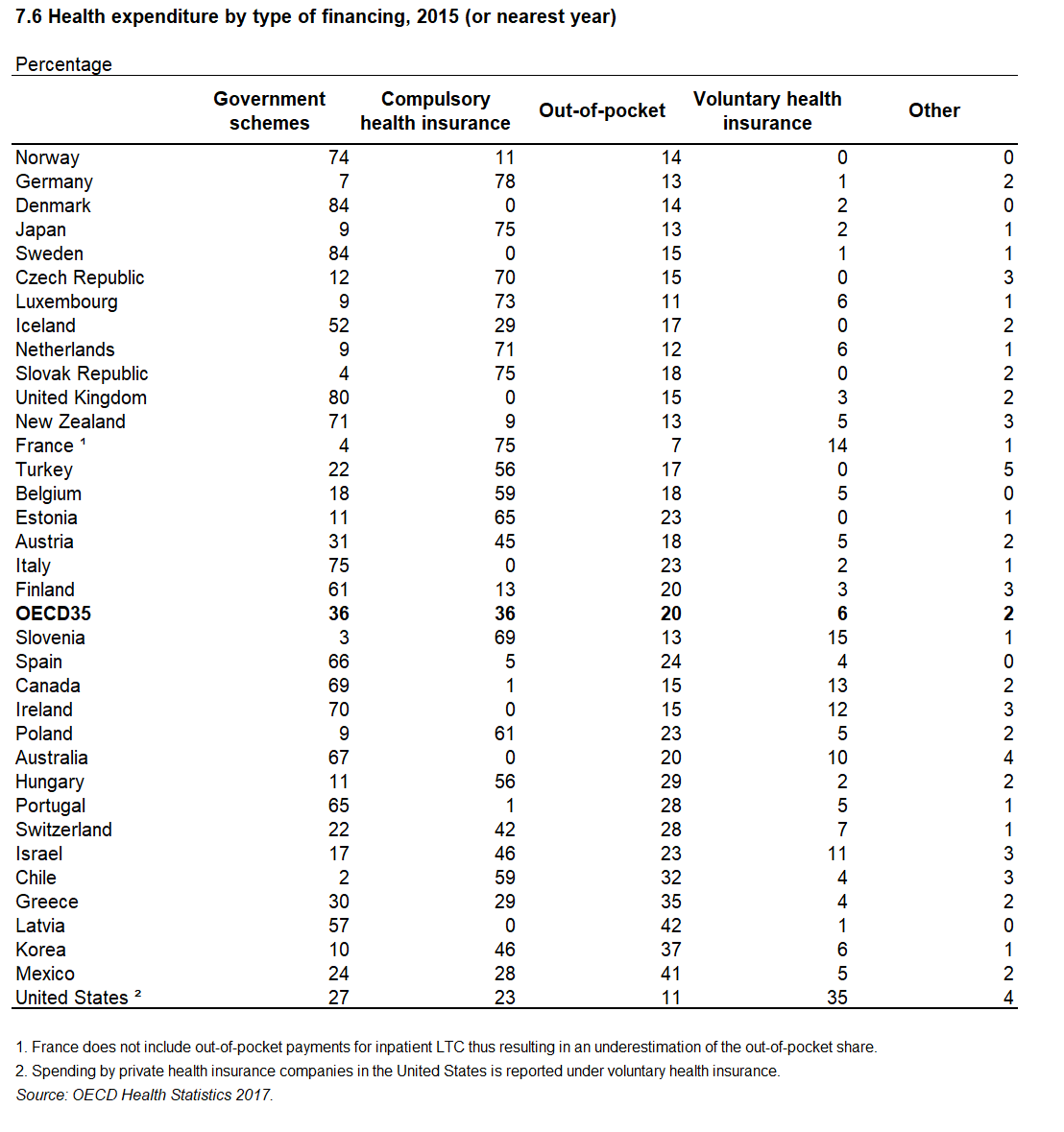

But it does matter what happens elsewhere. It is important to understand what “universal healthcare systems” actually look like in the rest of the world. In a prior article I shared an OCED chart on health care expenditures in developed countries, split by payor, and made some general comments on a number of countries.

So — getting back to my title — there is a real “Medicare for All” system in the world today, because “Medicare” is the name Australia gives its public healthcare system.

And according to that chart, Medicare covers 67% of healthcare costs. Who pays the rest?

20% comes from out-of-pocket charges. 10% comes from private health insurance, which nearly half (46%) of Australians elect. And 2% comes from “other” sources.

Here’s the scoop:

Australian Medicare covers public hospitals and doctor’s visits, as well as x-rays and other diagnostic tests, surgery, eye exams, some dental surgery, at a rate of 100% of the scheduled fee, for general practitioners and 85% of the scheduled fee for specialists. Doctors may choose to accept these rates as payment in full and bill Medicare directly, or if they charge in excess of these rates, bill patients directly, who then seek reimbursement from Medicare (for instance, through a mobile app) for the covered amounts, and pay the excess themselves. Medicare does not cover ambulance services, most dental care, most therapy services, glasses, hearing aids, or home nursing. Drugs are also only covered with a patient cost-share.

Private health insurance is a very popular option to cover these additional charges. In addition, Medicare-only patients cannot choose their own doctors, but private health insurance provides this option. Private health insurance also affords patients the ability to have a private room rather than a multi-bed room (shared with as many as five others), and to receive treatment, in general, at a private hospital, with charges equivalent to what public hospitals would cost, covered by Medicare, and the rest paid by the insurance/out of pocket. Finally, private health insurance allows patients to skip waiting lists. For example, public patients waiting for knee replacements waited for 203 days on average, but everyone else had a wait of 67 days. An Australian I know shared his personal experience when I said I was drafting an article:

The private insurance is essentially to get you to the front of the queue for elective or non essential surgery, or to get you a private room in a private or public hospital. It also helps a lot with the stuff that isn’t covered by Medicare.

As an example our son was 18 months old and barely saying a word. We applied through the public system for speech therapy but it was a 3 to 6 month waiting list. So we went to a private speech therapist and got seen within a week. The private health insurance covers part of the cost of speech therapy. In the end he was seeing both speech therapists because one was free on the public system and the other we weren’t out of pocket all that much for.

But as much as private insurance systems are reviled by single-payer promoters in the U.S., in Australia, the government encourages its citizens to purchase private health insurance, through the Medicare Levy Surcharge, an extra tax of 1% of income or more for anyone with over AUD 90,000 (about USD 64,000) in income without a private insurance policy, and through the Private Health Insurance Rebate, a means-tested government subsidy of 26% of the premium, for those with less than AUD 90,000 and younger than age 65, increasing to 36% for the older 70s, and phasing out to 0% at AUD 140,000.

One other noteworthy element of the Medicare system is that the government wholly circumvented any constitutional battles similar to what we’ve faced, by actually amending their constitution in1946, to give their federal government the power to provide hospital and medical services.

(Information on the system can be found at the following links: PrivateHealth.gov.au, the Australian Government Department of Human Services Medicare website, and Wikipedia. I also referenced two links provided by my Australian friend, “Benefits of Private Health Insurance,” and “Do you really need private health insurance? Here’s what you need to know before deciding,” which spell out some of the practicalities from an Australian perspective.)

This is the primary point I want to drive home: the dream of having the government pay for all healthcare consumed by its residents simply doesn’t exist. Markets for private-sector health insurance continue to exist even in “universal health care” countries, for multiple reasons. To refer back to the OECD chart, even among the most generous countries, government spending seems to top out at 85%, almost as if there’s some sort of economic law that means it’s simply not possible to exceed this. (And there is likewise not a communist utopia to point to, either, though that’s a subject for another time.)

“Medicare for All” advocates think this is a bad thing. In fact, it’s not.

Now, for the time being, I’m going to sidestep the question of whether any form of “Medicare for All” or “enhanced Obamacare” or whatever you’d like to call it, is a good idea in general.

However, if we take a shift to a more state-paid system as a given, a hybrid system solves many problems with respect to wait lists, rationing, etc., while still providing a base level of care to all.

Yet, at the same time, the demon of path dependency may well prevent it — not only in terms of the existing healthcare infrastructure (e.g., the new hospitals with all-private rooms, and semi-private the norm everywhere) and the untold number of employees who would not stand, politically, for losing their jobs or having their salaries halved, but also because of the expectation we have that, whatever might ail our system, wait lists or determinations that a procedure is not cost-effective are too high a price to pay.

Image: http://www.dodlive.mil/2017/10/03/usns-comfort-how-the-hospital-ship-helps-during-disasters/(U.S. Air Force photo by Staff Sgt. Courtney Richardson). public domain.